Ever wondered what the difference was between "Aggressive Growth" and "Ultra" funds? Well click here for the full explanation.

Excellent stuff - and quite funny unless you actually own one these things.

HT: Felix Salmon

Tuesday, December 15, 2009

Monday, December 14, 2009

Are stocks more risky in the long term

Are stocks more risky in the long term?

I'd guess that most investors think that stocks are actually safer in the long run than in the short run. This idea is supported by the well known book by Jeremy Siegel.

The intuition is based on a of time-based diversification - in the long run the ups and downs cancel themselves out.

But as Fama and French note, this logic suffers a fatal flaw. This time diversification effect only really works if you know what the true expected return is, and for stocks this is unknown. So, as the time horizon gets longer, you face risk from the volatility of the expected return, and also risk from not knowing what the expected return is.

Is Siegel's book wrong? The answer depends on how you view it. If you read it as a description of how well stocks did over the past 100 years, then it is a great read. If you think it tells us something concrete about the future, then I'd exercise more caution.

I'd guess that most investors think that stocks are actually safer in the long run than in the short run. This idea is supported by the well known book by Jeremy Siegel.

The intuition is based on a of time-based diversification - in the long run the ups and downs cancel themselves out.

But as Fama and French note, this logic suffers a fatal flaw. This time diversification effect only really works if you know what the true expected return is, and for stocks this is unknown. So, as the time horizon gets longer, you face risk from the volatility of the expected return, and also risk from not knowing what the expected return is.

Is Siegel's book wrong? The answer depends on how you view it. If you read it as a description of how well stocks did over the past 100 years, then it is a great read. If you think it tells us something concrete about the future, then I'd exercise more caution.

Sunday, December 13, 2009

RIP Paul Samuelson

The Economist, Paul Samuelson has died. My MBA students will recall his appearance in the "trillion dollar bet" in which he utters the wonderful line that he got Louis Bachelier's Thesis translated from French to English in order to "preserve every precious pearl".

Tuesday, December 1, 2009

Can you have positive alpha in an efficient market?

Is a positive alpha in an efficient market evidence of illegal activity?

I don't think so. There is nothing in the efficient market theory that says that an investor cannot earn positive alpha. In fact it is entirely possible for an investor to beat the market for many years in a row. Market efficiency just says that the reason for the investor's success was luck, not skill.

I don't think so. There is nothing in the efficient market theory that says that an investor cannot earn positive alpha. In fact it is entirely possible for an investor to beat the market for many years in a row. Market efficiency just says that the reason for the investor's success was luck, not skill.

Luck vs Skill in mutual fund management

Gene Fama and Ken French show that after you take account of fees, actively managed mutual funds underperform index funds. This is not new news really, but Fama and French present the evidence in an exhaustively robust way. The evidence against active management is very strong.

Felix Salmon summarizes the article nicely here.

Still, most investors will ignore the results of this and other similar studies and chase returns by trying to pick actively managed funds. In the long run they will fail.

Felix Salmon summarizes the article nicely here.

Still, most investors will ignore the results of this and other similar studies and chase returns by trying to pick actively managed funds. In the long run they will fail.

Tuesday, November 17, 2009

FF on duration, term structure and immunization

Great post on the Fama French blog about long term bonds.

Thursday, November 12, 2009

Call options and insider trading

My students know that options provide leverage. You don't have to exercise the option to profit, you just need to hold a call option while the stock price goes up. Your gain will be from the increase in the value of the option. My students also should know that insider trading is the practice of making trades based on private information.

So knowing all this, if you knew that HP was about to launch a takeover of 3COM, what would you do? Answer: buy calls on 3COM of course.* Turns out that's what a lot of people did.

*assuming you were willing to risk breaking the law.

So knowing all this, if you knew that HP was about to launch a takeover of 3COM, what would you do? Answer: buy calls on 3COM of course.* Turns out that's what a lot of people did.

*assuming you were willing to risk breaking the law.

Monday, November 9, 2009

Fama and French on portfolio optimization and the equity premium.

Fama and French talk about how to figure out the equity premium to use in a portfolio optimization problem. Excellent stuff and required reading for any finance MBA students!

Moral hazard and health care

Moral hazard is the term generally given to a situation where an individual does something that they normally would not do if they bore all the risk. There are many cases of moral hazard: For example, banks that lever up and take excessive risks but have implicit government guarantees are engaging in moral hazard.

The new health care plan that is making its way through the house prevents insurers from denying coverage based on a pre-existing condition. This is a great idea, but with it comes a moral hazard problem. Healthy people have the incentive to not get insurance until they get sick. Then they are guaranteed that they will be accepted into a plan. This doesn't just include the currently uninsured either. I have health insurance, but maybe I should drop my coverage and wait until I get really sick before reinstating it? I could save a huge amount. The economist, Martin Feldstein talks about the problem here.

The writers of the bill thought of this problem. Well sort of. They decided to impose a tax penalty on anyone who didn't get insurance. Brilliant! Except that the penalty is significantly less than the actual cost of insurance, so the problem does not go away.

I don't really want to get political here, but it seems to me that the problem with politicians is that they didn't take enough (or any) economics in school. In fact, if they had just read the book "Freakonomics" they would have seen an example of a very similar situation. I don't recall the exact details, but the basic story recounted in the book was that a day care center had a problem with parents being late to pick up their kids. To try to discourage this behavior, the day care center imposed a fine for each 30 minutes that the parents were late. The problem was that the fine was too low - well below the actual cost of child care. So instead of discouraging the behavior, more parents chose to be late and just pay the fine.

The solution to the health care moral hazard is simple. Make the penalty as much as the cost of insurance and force the non-insurers into a plan.

HT: Greg Mankiw's blog

The new health care plan that is making its way through the house prevents insurers from denying coverage based on a pre-existing condition. This is a great idea, but with it comes a moral hazard problem. Healthy people have the incentive to not get insurance until they get sick. Then they are guaranteed that they will be accepted into a plan. This doesn't just include the currently uninsured either. I have health insurance, but maybe I should drop my coverage and wait until I get really sick before reinstating it? I could save a huge amount. The economist, Martin Feldstein talks about the problem here.

The writers of the bill thought of this problem. Well sort of. They decided to impose a tax penalty on anyone who didn't get insurance. Brilliant! Except that the penalty is significantly less than the actual cost of insurance, so the problem does not go away.

I don't really want to get political here, but it seems to me that the problem with politicians is that they didn't take enough (or any) economics in school. In fact, if they had just read the book "Freakonomics" they would have seen an example of a very similar situation. I don't recall the exact details, but the basic story recounted in the book was that a day care center had a problem with parents being late to pick up their kids. To try to discourage this behavior, the day care center imposed a fine for each 30 minutes that the parents were late. The problem was that the fine was too low - well below the actual cost of child care. So instead of discouraging the behavior, more parents chose to be late and just pay the fine.

The solution to the health care moral hazard is simple. Make the penalty as much as the cost of insurance and force the non-insurers into a plan.

HT: Greg Mankiw's blog

Thursday, November 5, 2009

More on bank capital ratios

In my MBA class last night we watched "The Trillion Dollar Bet" about Long Term Capital Mgmt. I believe that a large part of LTCM's problem was not the bets they were taking but the leverage that they were using. The recent financial meltdown has, again been in large part due to excessive leverage.

Which brings us to the question of banks being too big to fail. Here's another blog arguing that we need capital ratios that increase with size. Very large banks that become too big to fail should hold very large amounts of capital.

For more discussion, see my recent post about about how implicit and explicit government guarantees encourage excessive leverage.

Which brings us to the question of banks being too big to fail. Here's another blog arguing that we need capital ratios that increase with size. Very large banks that become too big to fail should hold very large amounts of capital.

For more discussion, see my recent post about about how implicit and explicit government guarantees encourage excessive leverage.

Wednesday, November 4, 2009

Bank capital structure

The Economist has a nice article applying Modigliani and Miller's capital structure theory to the capital structure of banks. M&M said that in the absence of taxes and bankruptcy costs capital structure should not matter.

But banks are different - because large banks are too big to fail, the presence of bankruptcy costs don't matter. Furthermore, as banks benefit from very low debt costs (due to deposit insurance), their optimal capital structure is frequently very high.

In reality, large banks are more risky because of the risk they transfer to outsiders (tax payers) and therefore they should hold more capital than equivalent banks of a smaller size. But of course the banks don't want to hold more equity capital as equity is expensive relative to deposits.

The article is well worth a read.

But banks are different - because large banks are too big to fail, the presence of bankruptcy costs don't matter. Furthermore, as banks benefit from very low debt costs (due to deposit insurance), their optimal capital structure is frequently very high.

In reality, large banks are more risky because of the risk they transfer to outsiders (tax payers) and therefore they should hold more capital than equivalent banks of a smaller size. But of course the banks don't want to hold more equity capital as equity is expensive relative to deposits.

The article is well worth a read.

Another bubble coming?

Newsweek has a great article looking at whether we are in an "echo bubble". The takeaway: we are still in for a rough ride.

Is market efficiency the culprit?

Eugene Fama argues that market efficiency was not the reason for the financial crisis in this excellent posting on his blog.

Monday, November 2, 2009

Home buyer's credits

Jack Hough of Smartmoney doesn't like the proposed extension of the home buyers credit. Neither do I. I am not sure that I fully agree with all his points, but the first two are on target. A home buyer credit will have the effect of raising prices. I doubt very much that it will have significant stimulus effect.

May I suggest a better use for the money. If you want to stimulate the economy and increase employment, use the credit instead to reduce payroll taxes. You'll distribute the stimulus money evenly across the economy instead of just to a) new home buyers or b) people who want to trade their clunker for a prius.

May I suggest a better use for the money. If you want to stimulate the economy and increase employment, use the credit instead to reduce payroll taxes. You'll distribute the stimulus money evenly across the economy instead of just to a) new home buyers or b) people who want to trade their clunker for a prius.

Its always harder to dig out of the hole

As the Wall Street Journal discusses today, you need larger returns to get back to where you were before your portfolio suffered a loss.

The math is simple. Start with $100. Loose 50%. You've now got $50. To get back to $100 you need a 100% return.

Of course, you can get back quicker if you save more.

The math is simple. Start with $100. Loose 50%. You've now got $50. To get back to $100 you need a 100% return.

Of course, you can get back quicker if you save more.

Wednesday, October 28, 2009

Inflation and stock prices.

I've been checking out a new blog on Reuters by a Rolfe Winkler. It's pretty good, although his recent posting on inflation and stock prices makes the common mistake of confusing nominal and real growth rates. In economics parlance, we call this inflation or money illusion.

The basic error of inflation illusion is that a nominal discount rate is used to present value a firm's cash flows while a real growth rate is used to grow them. The result is that when inflation increases, the discount rate goes up and the present value of cash flows declines. This leads to the oft-cited conclusion that stock prices will decline when inflation increases.

In fact, stocks are natural hedges against inflation because the cash flows are real. This means that they increase with inflation. As prices go up, the firm's revenue and cash flows increase accordingly.

At the simplest level, consider the Dividend Discount Model.

P = D1/r-g

D1 is the dividend expected next year. r is the nominal discount rate and g is the growth rate. An increase in inflation will increase r through the risk free rate. g will also increase at the rate of inflation. Because the numerator is r-g, the effect of inflation will cancel out.

Mr Winkler is not alone in suffering from inflation illusion. The effect has been well documented. The original idea of inflation illusion affecting stock prices was proposed by Franco Modigliani and Richard Cohn in 1979. Since then, numerous academics have studied the issue and found evidence of inflation illusion. For example, John Campbell and Tuomo Vuolteenaho find evidence in their American Economic Review paper in 2004. Yours truly also found evidence for inflation illusion in my 2002 Journal of Financial and Quantitative Analysis with Jay Ritter.

Inflation illusion also affects house prices, but that's a topic for another day...

The basic error of inflation illusion is that a nominal discount rate is used to present value a firm's cash flows while a real growth rate is used to grow them. The result is that when inflation increases, the discount rate goes up and the present value of cash flows declines. This leads to the oft-cited conclusion that stock prices will decline when inflation increases.

In fact, stocks are natural hedges against inflation because the cash flows are real. This means that they increase with inflation. As prices go up, the firm's revenue and cash flows increase accordingly.

At the simplest level, consider the Dividend Discount Model.

P = D1/r-g

D1 is the dividend expected next year. r is the nominal discount rate and g is the growth rate. An increase in inflation will increase r through the risk free rate. g will also increase at the rate of inflation. Because the numerator is r-g, the effect of inflation will cancel out.

Mr Winkler is not alone in suffering from inflation illusion. The effect has been well documented. The original idea of inflation illusion affecting stock prices was proposed by Franco Modigliani and Richard Cohn in 1979. Since then, numerous academics have studied the issue and found evidence of inflation illusion. For example, John Campbell and Tuomo Vuolteenaho find evidence in their American Economic Review paper in 2004. Yours truly also found evidence for inflation illusion in my 2002 Journal of Financial and Quantitative Analysis with Jay Ritter.

Inflation illusion also affects house prices, but that's a topic for another day...

Friday, October 23, 2009

Air freight and stock prices...

In my undergrad investments class we've been talking about efficient markets and how new information arrival is random. This new information is then rapidly incorporated into stock prices.

Here's an interesting example. On Monday Apple reported its quarterly earnings and let slip that it is paying for abnormally high air freight that is not iphone related.

Hmmm, what could this be for?

Of course, analysts are speculating that the company is prepping for the imminent release of a tablet computer.

This is a perfect example of new information that was not expected by the market, but that would have a material effect on the stock price.

Here's an interesting example. On Monday Apple reported its quarterly earnings and let slip that it is paying for abnormally high air freight that is not iphone related.

Hmmm, what could this be for?

Of course, analysts are speculating that the company is prepping for the imminent release of a tablet computer.

This is a perfect example of new information that was not expected by the market, but that would have a material effect on the stock price.

Monday, October 19, 2009

Google's bandwidth bill is probably not zero.

Here's a good question for finance students. Based on this article, is Google's bandwidth bill for youtube really zero?

The article argues that Google has soooo much fiber optic cable that it basically trades bandwidth with other ISPs and never pays for bandwidth. So if you're doing a cash flow analysis on youtube would assume that band width cost was really zero?

For a bonus, use the words "opportunity cost" and "sunk cost" correctly in your answer.

The article argues that Google has soooo much fiber optic cable that it basically trades bandwidth with other ISPs and never pays for bandwidth. So if you're doing a cash flow analysis on youtube would assume that band width cost was really zero?

For a bonus, use the words "opportunity cost" and "sunk cost" correctly in your answer.

What about China and the US Government debt?

Twice in the past couple of weeks I have been at some social event (usually involving beer) and have been asked "what about China and all the US debt it keeps buying?"

This article discusses the issue nicely.

I also need to drink beer with less serious people.

HT: Greg Mankiw

This article discusses the issue nicely.

I also need to drink beer with less serious people.

HT: Greg Mankiw

Smart guys on wall street...

Q. What caused the financial meltdown?

A. Too many smart guys on wall street.

Or so says this entertaining article...

HT: My friend Robert

A. Too many smart guys on wall street.

Or so says this entertaining article...

HT: My friend Robert

Thursday, October 15, 2009

A candid interview with a banker

Excellent stuff courtesy of the Financial Times. 10 minutes long, but pretty entertaining.

Monday, October 12, 2009

Trouble with stock options, part deux

We've heard plenty about the option backdating scandal in which firms retroactively awarded stock options at the lowest stock price of the quarter.

Well now there appears to be a new, but related scandal brewing. The WSJ discusses a new study by Fich, Cai and Tran at Drexel U. who find that firms that are in merger negotiations are pretty liberal with their option grants.

They allege that when negotiations about a merger are being quietly made, the target firm grants options to the CEO of the target. Then, when the merger is announced the stock price will most likely go up and the CEO makes out.

One possible explanation is that you want to incent the CEO to get the best possible price from the merger, and options will do that. But as is pointed out in the article, the CEO's pay package should already provide the correct incentives if it is well constructed.

.

Well now there appears to be a new, but related scandal brewing. The WSJ discusses a new study by Fich, Cai and Tran at Drexel U. who find that firms that are in merger negotiations are pretty liberal with their option grants.

They allege that when negotiations about a merger are being quietly made, the target firm grants options to the CEO of the target. Then, when the merger is announced the stock price will most likely go up and the CEO makes out.

One possible explanation is that you want to incent the CEO to get the best possible price from the merger, and options will do that. But as is pointed out in the article, the CEO's pay package should already provide the correct incentives if it is well constructed.

.

High Frequency Trading and the small investor

High frequency trading is the process of using powerful computers to exploit the smallest inefficiencies in stock prices. The Wall Street Journal has a good primer on the topic here.

One of the problems of HFT is that the little guy can get mowed down by the massive trades put on by HFT algorithms. Matthew Goldstein of Reuters discusses one such case.

As my undergrad students should know, a stop loss order is really just a market order to sell that is waiting to be triggered. The key risks with a stop loss is that it will either get triggered by a gyration in the stock or that it will trigger far below the original order price because the stock is moving so fast. This is precisely what happened in the case discussed by Goldstein, who says...

What to take away? If you are an individual investor trading stocks on your own, you are swimming with the sharks. Nothing good will come of it. You should be indexing.

HT: Felix Salmon

One of the problems of HFT is that the little guy can get mowed down by the massive trades put on by HFT algorithms. Matthew Goldstein of Reuters discusses one such case.

As my undergrad students should know, a stop loss order is really just a market order to sell that is waiting to be triggered. The key risks with a stop loss is that it will either get triggered by a gyration in the stock or that it will trigger far below the original order price because the stock is moving so fast. This is precisely what happened in the case discussed by Goldstein, who says...

The lightening fast selling triggered a so-called stop-loss standing order Watson had with his broker to sell Dendreon shares if the stock fell into the low $20s. But the stock fell so fast that the broker didn’t actually sell Watson’s 1,500 shares until the price had hit $15

What to take away? If you are an individual investor trading stocks on your own, you are swimming with the sharks. Nothing good will come of it. You should be indexing.

HT: Felix Salmon

Saturday, October 10, 2009

How risky are stocks?

The widely held view that stocks are not risky in the long run is attacked by a nice article in today's WSJ.

It states:

It states:

Look at the long-term average annual rate of return on stocks since 1926, when good data begin. From the market peak in 2007 to its trough this March, that long-term annual return fell only a smidgen, from 10.4% to 9.3%. But if you had $1 million in U.S. stocks on Sept. 30, 2007, you had only $498,300 left by March 1, 2009. If losing more than 50% of your money in a year-and-a-half isn't risk, what is?

Executive Pay

David Yermack, an NYU finance prof, has an excellent article in today's WSJ about executive pay. Yermack has been critical in the past of executive compensation - he wrote a very interesting article about the uses and abuses of corporate jets.

His article today makes a simple and often overlooked point. You have to include the value of past stock and option grants when figuring out how execs are compensated. You cannot just focus on this year's salary.

Many executives lost massive amounts of personal wealth when their company stock prices collapsed. No one feels bad for them as this is true pay for performance. Shareholders lost money and so did they.

Overall Yermack concludes that CEO compensation contracts work pretty well and the current witch hunt, which might be good for the media and some political careers, really won't make things better.

His article today makes a simple and often overlooked point. You have to include the value of past stock and option grants when figuring out how execs are compensated. You cannot just focus on this year's salary.

Many executives lost massive amounts of personal wealth when their company stock prices collapsed. No one feels bad for them as this is true pay for performance. Shareholders lost money and so did they.

Overall Yermack concludes that CEO compensation contracts work pretty well and the current witch hunt, which might be good for the media and some political careers, really won't make things better.

Thursday, October 8, 2009

Nobel Prize for Economics

Given that the Nobel for Economics is to be announced on Monday, I thought it might be nice to see who has won it in the past...

Here's the list

Here's the list

Wednesday, October 7, 2009

Do TIPs provide inflation protection...?

TIPS - Treasury Inflation Protected Bonds are designed to provide inflation protection to investors. These US government bonds have par values that increase at the rate of the CPI each year. Because the par value increases, the coupon payment also increases. Thus the payment you get is, in effect, indexed to inflation.

Jeff Opdyke of The Wall Street Journal asks - "do these bonds provide inflation protection?" Its a good question, however I think that Opdyke's analysis has some problems.

First he points to the fact that the CPI is an imperfect measure of inflation. This is absolutely true, for example the CPI doesn't include extra bag fees for airlines. But I disagree that a flaw in the index is that it doesn't include borrowing costs. The CPI specifically doesn't include borrowing costs, in part because using a cost that is directly related to inflation in the index would lead to a feedback loop. Furthermore, when mortgage rates increase, the higher borrowing costs are offset by house price appreciation - so it is unclear whether a household's costs have truly increased.

A second point raised is that if you sell the bonds before they mature, you are not guaranteed the promised return. As my students should know, this is incorrect. To earn the initial yield to maturity you need to hold bonds whose duration is equal to your holding period. Holding the bonds to their maturity exposes you to reinvestment risk from the coupons. Zvi Bodie has talked about this issue and advocates target date duration matched TIPs funds for retirement.

Finally, Opdyke argues that 3% tips would underperform 5% tips in an environment where rates increase. We have to be careful here. If the rate increase is just due to higher inflation, then there will be no difference in the real return on these bonds. But if the increase reflects a higher real rate of interest, then the lower coupon bonds will be hurt more because they have a higher duration.

Overall though, this is an interesting article and well worth a read.

Jeff Opdyke of The Wall Street Journal asks - "do these bonds provide inflation protection?" Its a good question, however I think that Opdyke's analysis has some problems.

First he points to the fact that the CPI is an imperfect measure of inflation. This is absolutely true, for example the CPI doesn't include extra bag fees for airlines. But I disagree that a flaw in the index is that it doesn't include borrowing costs. The CPI specifically doesn't include borrowing costs, in part because using a cost that is directly related to inflation in the index would lead to a feedback loop. Furthermore, when mortgage rates increase, the higher borrowing costs are offset by house price appreciation - so it is unclear whether a household's costs have truly increased.

A second point raised is that if you sell the bonds before they mature, you are not guaranteed the promised return. As my students should know, this is incorrect. To earn the initial yield to maturity you need to hold bonds whose duration is equal to your holding period. Holding the bonds to their maturity exposes you to reinvestment risk from the coupons. Zvi Bodie has talked about this issue and advocates target date duration matched TIPs funds for retirement.

Finally, Opdyke argues that 3% tips would underperform 5% tips in an environment where rates increase. We have to be careful here. If the rate increase is just due to higher inflation, then there will be no difference in the real return on these bonds. But if the increase reflects a higher real rate of interest, then the lower coupon bonds will be hurt more because they have a higher duration.

Overall though, this is an interesting article and well worth a read.

Tuesday, September 29, 2009

What to do when a cell phone rings during class...

From the BBC website. Act cool like Hugh Jackman.

Friday, September 25, 2009

Google's option repricing.

Today the Wall Street Journal talks about the huge windfall that Google's employees received because the company repriced their stock options back in March.

At the time, Google argued that it was only fair to reset the strike price of the options because so many of them were so far out of the money due to the stock market collapse. Google wasn't alone. On March 23 Bloomberg reports that a range of companies were doing this.

When Google reset the options, the price of the stock was at $308, today the price is at $494. In effect Google orchestrated a massive wealth transfer from shareholders to employees. We're not talking chump change here either. The WSJ estimates the transfer was around $1.5 billion.

Their argument that they wanted to retain the best just doesn't fly. Would you quit your job with Google in the middle of the worst recession in 80 years?

As the Wall Street Journal points out, "Google is a different kind of company" - yes - one that gleefully fleeces its own shareholders.

At the time, Google argued that it was only fair to reset the strike price of the options because so many of them were so far out of the money due to the stock market collapse. Google wasn't alone. On March 23 Bloomberg reports that a range of companies were doing this.

When Google reset the options, the price of the stock was at $308, today the price is at $494. In effect Google orchestrated a massive wealth transfer from shareholders to employees. We're not talking chump change here either. The WSJ estimates the transfer was around $1.5 billion.

Their argument that they wanted to retain the best just doesn't fly. Would you quit your job with Google in the middle of the worst recession in 80 years?

As the Wall Street Journal points out, "Google is a different kind of company" - yes - one that gleefully fleeces its own shareholders.

Thursday, September 24, 2009

Finance Films

The Economist has a blog posting talking about finance films. The conclusion is that overall, they tend to be not very good.

The comments on the post make for interesting reading and perhaps might contain a few suggestions for your netflix queue.

My personal faves are

Boiler room

Wall Street

Barbarians at the Gate

Rogue trader

Feel free to post any that I might have missed (as comments).

The comments on the post make for interesting reading and perhaps might contain a few suggestions for your netflix queue.

My personal faves are

Boiler room

Wall Street

Barbarians at the Gate

Rogue trader

Feel free to post any that I might have missed (as comments).

Wednesday, September 23, 2009

Sensationalist Wall Street Journal

Felix Salmon argues that the Wall Street Journal is taking a turn for the worse under its new ownership by using sensationalist headlines. I think he has a point. You used to be able to rely on the WSJ for pretty unbiased solid coverage of financial news. Now there seems to be an underlying agenda.

Financial Times Alphaville

FT Alphaville is a blog sponsored by the Financial Times, which is the UK equivalent of the Wall Street Journal except that it is not owned by Rupert Murdoch.

The blog is updated from London, New York and Tokyo and is designed to be a 24 hour news service. Its free - and also provides links to other blogs as well as the FT. I'll be adding it to my blog reader.

The blog is updated from London, New York and Tokyo and is designed to be a 24 hour news service. Its free - and also provides links to other blogs as well as the FT. I'll be adding it to my blog reader.

Monday, September 21, 2009

Front running a merger

Saturday, September 19, 2009

Tariffs on tires are a bad idea.

The Economist is unimpressed with the latest round of trade tariffs on tires (or tyres) as they say across the pond.

Pick 3 lottery stupidity

The NC education lottery is designed to generate funds for NC schools. Whether or not it is effective in that goal is debatable, but what it really is, is a tax on the mathematically challenged.

Exhibit A: The triangle troubleshooter (a column in the Raleigh News and Observer) reports the terrible wrong done to a poor woman who purchased 2 "Pick Three" tickets and, shock, horror, got the same number on both tickets. Oh the humanity...

The classic line from the lottery player is

Consider the facts - its a pick THREE. There are 1000 possible numbers (assuming you allow 000), and 581,468 tickets are sold.

I propose that all proceeds from the lottery be directed to teach the citizens of this great state the basics of probability theory.

But until that happens, don't play the lottery unless a) you are severely mathematically challenged or b) you don't feel like you pay enough state tax.

Exhibit A: The triangle troubleshooter (a column in the Raleigh News and Observer) reports the terrible wrong done to a poor woman who purchased 2 "Pick Three" tickets and, shock, horror, got the same number on both tickets. Oh the humanity...

The classic line from the lottery player is

"I don't have faith in this system," she said. "It doesn't make sense to me mathematically. There should be enough numbers that each ticket would be individual."

Consider the facts - its a pick THREE. There are 1000 possible numbers (assuming you allow 000), and 581,468 tickets are sold.

I propose that all proceeds from the lottery be directed to teach the citizens of this great state the basics of probability theory.

But until that happens, don't play the lottery unless a) you are severely mathematically challenged or b) you don't feel like you pay enough state tax.

Wednesday, September 16, 2009

What do economists think?

Greg Mankiw posts a link to "what economists believe". Take a look and see if you agree!

Mankiw also mentions the recent tire tariffs imposed by President Obama on Chinese tires. Most economists think tariffs are a very bad idea (me included). It does make you wonder though why new Presidents are so quick to levy tariffs. For example, GWB did a similar thing in 2002.

Mankiw also mentions the recent tire tariffs imposed by President Obama on Chinese tires. Most economists think tariffs are a very bad idea (me included). It does make you wonder though why new Presidents are so quick to levy tariffs. For example, GWB did a similar thing in 2002.

The price is right and the EMH

The Guardian has a short article talking about two components of the EMH (Efficient Market Hypothesis).

The conclusion is slightly amusing.

The conclusion is slightly amusing.

But that still leaves the first part of EMH intact; that you can't beat the market unless you have insider information. It implies that most of us are better off stowing our savings in a cheap fund that tracks the stock market, rather than with some expensive smarty-pants fund manager. There you go, an idea from economics that might save you money: who'd have thought it?

Tuesday, September 15, 2009

How did economists get it wrong?

Well, first you have to accept the premise of the title, but assuming that you do (and even if you don't), Paul Krugman has a lengthy article on the evolution of macroeconomics and how it relates to the current situation. I don't know whether I buy it all, but I'm not a macro-economist and I don't have a Nobel prize.

HT: My friend Bill.

HT: My friend Bill.

Did Lehman's collapse start the crisis?

Two very reputable economists from Chicago, John Cochrane and Luigi Zingales suggest that the true cause of the crash probably has more to do with the TARP authorization...as they eloquently state...

HT: Greg Mankiw

In effect, these speeches [about TARP] amounted to "The financial system is about to collapse. We can't tell you why. We need $700 billion. We can't tell you what we're going to do with it." That's a pretty good way to start a financial crisis.

HT: Greg Mankiw

Friday, September 11, 2009

Healthcare in the UK

With all the talk about healthcare reform, the topic of systems in other countries crops up a lot. For example, Britain's NHS is frequently portrayed as a disaster by the media in the US.

This short documentary (again on Frontline) talks about the UK system. This is clearly not the solution for the US, but I think it indicates that there are, perhaps, alternatives that work pretty well. As always, its all about getting the incentives right.

This short documentary (again on Frontline) talks about the UK system. This is clearly not the solution for the US, but I think it indicates that there are, perhaps, alternatives that work pretty well. As always, its all about getting the incentives right.

Breaking the bank...

Breaking the Bank is an excellent documentary on PBS (produced by Frontline) that documents the hour by hour collapse of Lehman and the back room deals done as more banks imploded. A lot of focus is paid on the buyout of Merrill by B of A, which started out as a great deal until the true state of the mess that was Merrill's balance sheet became apparent.

You can watch it online, and I strongly recommend it to all my students. My only disagreement with the documentary was in the closing minutes where it is stated that basically the whole mess was Wall Street's fault, and now the Feds are running the show. I fundamentally disagree with this take. I, like many (or most) other economists put a large amount of the blame for the mess not on the lack of government regulation, but on the very poor and misguided regulation that encouraged subprime lending and allowed firms to abdicate their responsibility for risk management.

Anyhow, check out the show, its compelling viewing.

You can watch it online, and I strongly recommend it to all my students. My only disagreement with the documentary was in the closing minutes where it is stated that basically the whole mess was Wall Street's fault, and now the Feds are running the show. I fundamentally disagree with this take. I, like many (or most) other economists put a large amount of the blame for the mess not on the lack of government regulation, but on the very poor and misguided regulation that encouraged subprime lending and allowed firms to abdicate their responsibility for risk management.

Anyhow, check out the show, its compelling viewing.

Thursday, September 10, 2009

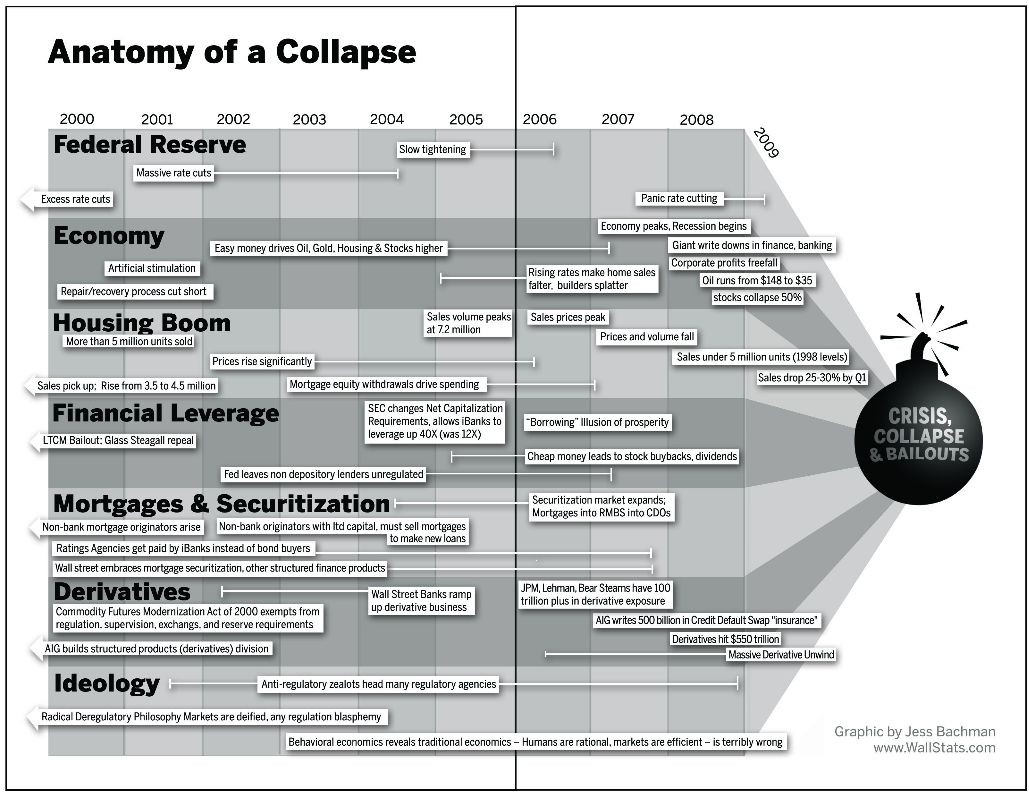

Follow the events that lead to the financial crisis

The BBC has another nice graphic showing a time line of events..

Wednesday, September 9, 2009

Alan Greenspan - it will happen again...

The ex-fed chief talks about the current mess and the likelihood of it happening again.

The cost of the financial meltdown

An interesting graphic from the BBC. The UK doesn't look too healthy.

Powerpoint

My colleague, Craig Newmark, posts a link to another critique of PowerPoint. I actually don't use PPT in my lectures. I used to, but I found that I was boring myself. I am sure some folks can use it creatively, but it is so easy for it to become a crutch.

Tuesday, September 8, 2009

The new auto industry breakdown

Just in case you weren't keeping up on all the changes to the US auto industry, here's a handy graphic to bring you up to speed.

Friday, September 4, 2009

Linux and high frequency trading.

Its not often that you find an article about linux (I am a user), stock trading, and a local company here in Raleigh (Red Hat).

Its all a bit geeky, but if you're so inclined, read on. Apparently RedHat Linux powers the world's fastest stock exchange.

Incidentally, I use ubuntu linux.

Its all a bit geeky, but if you're so inclined, read on. Apparently RedHat Linux powers the world's fastest stock exchange.

Incidentally, I use ubuntu linux.

The problems with alpha...

In my MBA class this semester, we haven't gotten to alpha yet... but this post on the unknown professor's blog touches on the weakness of alpha. The whole video is worth watching.

The source of the video is "falkenblog", and a more detailed post on the topic is here.

The quote:

made me laugh out loud.

The source of the video is "falkenblog", and a more detailed post on the topic is here.

The quote:

One should remember that Enron was the subject of Harvard Business School case studies in 'best practices' management, they emphasized their 'risk management' and received plaudits there.

made me laugh out loud.

CNBC - it makes my head hurt

The dumbest TV presenters are not on the afternoon chat shows, they are on CNBC. The Self-Evident blog has an excellent post on the latest CNBC idiocy.....

My favorite quote "I don't understand how that relates to what Larry was saying" - right because you are STUPID.

Actually for pure comedy value, CNBC is excellent.

My favorite quote "I don't understand how that relates to what Larry was saying" - right because you are STUPID.

Actually for pure comedy value, CNBC is excellent.

Thursday, August 27, 2009

Finance Fallacy #1

OK, Here is fallacy #1 - saving is not investing. I don't think I would list this as number 1, as I think we are stepping into the realm of semantics a little here.

Finance Fallacy #2

In light of my recent post on "stocks for the long run" Zvi Bodie argues why the idea of "stocks for the long run" is flawed. Transcript and audio is here

His basic idea, which is not new, he's been harping on it for a long time, is that stocks will on average beat bonds, but only on average. This means that the average investor will do OK investing in stocks for their retirement. But some investors will do a lot better than average and some will be do terribly (and end up eating dog food in their old age, as Zvi elegantly states). As an individual investor has only one shot at getting it right, being right on average is not too helpful.

Definitely worth listening to.

Incidentally, this is finance fallacy number 2, I'll have to look up what #1 is.

His basic idea, which is not new, he's been harping on it for a long time, is that stocks will on average beat bonds, but only on average. This means that the average investor will do OK investing in stocks for their retirement. But some investors will do a lot better than average and some will be do terribly (and end up eating dog food in their old age, as Zvi elegantly states). As an individual investor has only one shot at getting it right, being right on average is not too helpful.

Definitely worth listening to.

Incidentally, this is finance fallacy number 2, I'll have to look up what #1 is.

Hedge Fund Letters

Ever wanted to know what a hedge fund manager thinks?...Felix Salmon posts links to two hedge fund letters. Interesting stuff.

Socially useless banks?

From the Guardian newspaper... Lord Turner (top financial regulator in the UK) wants to tax "excessive profiteering" by "socially useless banks" in the UK.

All this sounds like a slippery slope to me. What is "excessive" and does he really think that banks are "socially useless"? He also talks about "simplistic regulation". I don't think it was lack of regulation that lead to the particularly bad financial mess in the UK, just bad regulation. In particular, the government took the implicit role of lender of last resort to banks that are too big to fail. Instead, the government should regulate capital standards that are a function of the bank size.

Elsewhere in the article Turner questions whether the financial sector has grown too large. In a free market, capital will move to the the most productive use. In the UK, this turns out to be the financial sector, in part because there isn't much in the way of a significant manufacturing sector anymore. The only way that I could conceive that the financial sector was "too large" is if it is receiving some sort of government subsidy, such as an implicit guarantee. In which case, we know who to blame.

All this sounds like a slippery slope to me. What is "excessive" and does he really think that banks are "socially useless"? He also talks about "simplistic regulation". I don't think it was lack of regulation that lead to the particularly bad financial mess in the UK, just bad regulation. In particular, the government took the implicit role of lender of last resort to banks that are too big to fail. Instead, the government should regulate capital standards that are a function of the bank size.

Elsewhere in the article Turner questions whether the financial sector has grown too large. In a free market, capital will move to the the most productive use. In the UK, this turns out to be the financial sector, in part because there isn't much in the way of a significant manufacturing sector anymore. The only way that I could conceive that the financial sector was "too large" is if it is receiving some sort of government subsidy, such as an implicit guarantee. In which case, we know who to blame.

Tuesday, August 25, 2009

Liar's Poker

I just finished reading Liar's Poker. Its one of those books that I should have read years ago, but I just never got around to it. For the handful of folks who haven't read it, it is a true story of someone spending two years at Salomon Brothers in the 1980s. Its a great book, but reveals the rather ugly side of the investment banking world. I'd like to think things are all different now, 20 years later, but I seriously doubt it.

Bonds for the long run?

A few years back, Jeremy Siegel of the Wharton wrote a book called "stocks for the long run". The basic premise of the book was that over long periods - stocks beat bonds. He showed that for pretty much any 30 year period in history this was true.

Unfortunately, many people misunderstood the basic idea. They assumed that stocks HAD to beat bonds over 30 year periods. This is absolutely not the case, all Siegel is saying is that they have, historically done so.

Incidentally, I highly recommend his book.

Which brings me to an excellent post on the Fama French Forum in which someone asks whether bonds will continue to beat stocks....read here.

FF's answer is really insightful. The key point here is to understand the difference between an expected risk premium and a realized risk premium.

As an analogy, confusing a realized risk premium and an expected risk premium is like thinking that it is a good time to buy beach property after a 100 year hurricane (as long as you sell within 100 years)!

Unfortunately, many people misunderstood the basic idea. They assumed that stocks HAD to beat bonds over 30 year periods. This is absolutely not the case, all Siegel is saying is that they have, historically done so.

Incidentally, I highly recommend his book.

Which brings me to an excellent post on the Fama French Forum in which someone asks whether bonds will continue to beat stocks....read here.

FF's answer is really insightful. The key point here is to understand the difference between an expected risk premium and a realized risk premium.

As an analogy, confusing a realized risk premium and an expected risk premium is like thinking that it is a good time to buy beach property after a 100 year hurricane (as long as you sell within 100 years)!

Meir Statman on Behavioral Finance

Meir Statman (finance Prof at UC Santa Clara) has a nice article in the Wall Street Journal talking about many of the common behavioral mistakes that investors make. Hopefully some of my past MBA students recall me talking about this in my Portfolio and Security Analysis class.

Saturday, August 22, 2009

Thursday, August 20, 2009

Perfect markets

I've not been blogging for the past few weeks as I've been taking a break - vacation etc. Anyhow, the fall semester is up and running and its time to get back at it!

A recent article in the New Scientist (a UK publication) really illustrates how people - even very smart scientists just don't get economics.

In the article "Falling out of love with market myths", Terence Kealey (vice chancellor at the University of Buckingham, UK) attacks the economics concept of a perfect market.

I'd like to take a moment to explain why he is completely wrong.

In financial economics, we frequently talk and think about things in terms of perfect markets. Usually a perfect market is one with full information to all participants and no frictions (such as trading costs or taxes).

Mr Kealey argues that perfect markets are "bizarre" and that the theory, and the efficient market theory are "false".

Unfortunately, Mr Kealey just doesn't understand what the purpose is of a perfect market. In finance, we don't think for a minute that markets are perfect. They are not, there are taxes, trading costs, regulation, information asymmetries etc. But by starting with an idea of what a perfect market would look like, we are able to more fully understand the distortions that market imperfections are likely to play. Perfect markets are used as the foundation of more complex theories that attempt to explain how the world really is, and more importantly, how it will change if we change the imperfections in the market.

Students might note that in introductory MBA finance, we start with perfect markets when considering capital structure and also asset pricing.

Notwithstanding this fairly poor article, the New Scientist is an excellent publication.

A recent article in the New Scientist (a UK publication) really illustrates how people - even very smart scientists just don't get economics.

In the article "Falling out of love with market myths", Terence Kealey (vice chancellor at the University of Buckingham, UK) attacks the economics concept of a perfect market.

I'd like to take a moment to explain why he is completely wrong.

In financial economics, we frequently talk and think about things in terms of perfect markets. Usually a perfect market is one with full information to all participants and no frictions (such as trading costs or taxes).

Mr Kealey argues that perfect markets are "bizarre" and that the theory, and the efficient market theory are "false".

Unfortunately, Mr Kealey just doesn't understand what the purpose is of a perfect market. In finance, we don't think for a minute that markets are perfect. They are not, there are taxes, trading costs, regulation, information asymmetries etc. But by starting with an idea of what a perfect market would look like, we are able to more fully understand the distortions that market imperfections are likely to play. Perfect markets are used as the foundation of more complex theories that attempt to explain how the world really is, and more importantly, how it will change if we change the imperfections in the market.

Students might note that in introductory MBA finance, we start with perfect markets when considering capital structure and also asset pricing.

Notwithstanding this fairly poor article, the New Scientist is an excellent publication.

Tuesday, August 4, 2009

A break down of the equity risk premium

Is the equity risk premium actually zero? This post makes this claim. The author argues for a range of reasons why a risk premium is less than the typical quoted number of 6%.

I am inclined to agree that it is less than 6%, but I think it is probably incorrect to say it is zero.

I have a few issues with some of his arguments:

1.He claims that various studies have shown that the risk premium is declining, particularly since the 2000 market crash. The problem here is that I think he is confusing survey evidence of peoples expectations of the market risk premium with the implied premium that actually generates current prices. Before the market crash, in the late 90s, most investors thought stocks were great, would give high returns, and therefore would expect a high return over bonds. But of course, stocks were very expensive then and the implied premium was very low. After the crash the opposite occurs. Investors think stocks are awful, and expect low returns, but as prices are low, the implied premium is high.

2. He argues that transaction costs are ignored. But the evidence for bid-ask spread induced costs that he quotes are largely from pre-decimilization, when spreads were much higher than they are now. I agree that frequent trading will eat returns, but I don't see how this is really relevant to the equity premium. Nor do I see how poor market timing will impact the equity premium. Both of these factors will impact realized returns, but the equity premium is a fairly refined concept of the return you will earn as a buy and hold investor holding the market portfolio. In essence, someone how has an index fund in his/her 401k.

3. He states that the geometric mean will be much lower than the arithmetic mean due to volatility. No argument here, but this is a straw man as no reasonable person uses the arithmetic mean to estimate historic returns.

4. Peso problem. I completely agree that the US is a special case in that it has posted one of the highest historic premiums of any country. There is no reason to believe that the US should not mean revert to the average of the developed world.

So what is the correct premium? I sort of skirted around this issue here. But I think it is somewhere between say 2-6%. But don't quote me on that.

Finally, what would a zero percent premium mean? Well I doubt it will be along the lines of the Dow trading to 36000..

I am inclined to agree that it is less than 6%, but I think it is probably incorrect to say it is zero.

I have a few issues with some of his arguments:

1.He claims that various studies have shown that the risk premium is declining, particularly since the 2000 market crash. The problem here is that I think he is confusing survey evidence of peoples expectations of the market risk premium with the implied premium that actually generates current prices. Before the market crash, in the late 90s, most investors thought stocks were great, would give high returns, and therefore would expect a high return over bonds. But of course, stocks were very expensive then and the implied premium was very low. After the crash the opposite occurs. Investors think stocks are awful, and expect low returns, but as prices are low, the implied premium is high.

2. He argues that transaction costs are ignored. But the evidence for bid-ask spread induced costs that he quotes are largely from pre-decimilization, when spreads were much higher than they are now. I agree that frequent trading will eat returns, but I don't see how this is really relevant to the equity premium. Nor do I see how poor market timing will impact the equity premium. Both of these factors will impact realized returns, but the equity premium is a fairly refined concept of the return you will earn as a buy and hold investor holding the market portfolio. In essence, someone how has an index fund in his/her 401k.

3. He states that the geometric mean will be much lower than the arithmetic mean due to volatility. No argument here, but this is a straw man as no reasonable person uses the arithmetic mean to estimate historic returns.

4. Peso problem. I completely agree that the US is a special case in that it has posted one of the highest historic premiums of any country. There is no reason to believe that the US should not mean revert to the average of the developed world.

So what is the correct premium? I sort of skirted around this issue here. But I think it is somewhere between say 2-6%. But don't quote me on that.

Finally, what would a zero percent premium mean? Well I doubt it will be along the lines of the Dow trading to 36000..

Wednesday, July 22, 2009

S&P at your finger tips

Political calculations has two excellent calculators online that show the performance of the S&P 500 over different time periods and also the amount you'd make by investing in the index over different time periods. Excellent stuff.

HT: FinanceProfessor.

HT: FinanceProfessor.

Tuesday, July 21, 2009

Inflation illusion at the movies

Inflation illusion is usually defined as the failure to take account of inflation. Not too surprisingly, it turns out that movie box office numbers suffer from inflation illusion. Consider this report on "the Hangover". Apparently the Hangover is the biggest R rated comedy of all time. It has grossed $235 Million, eclipsing Beverly Hills Cop in 1984 at $234 Million.

Of course, these numbers are like apples and oranges. The CPI in 1984 was 105.3 today it is 215.693. To convert BHC to todays numbers we multiply 234 by 215.693 and divide by 105.3. This gives us a whopping $479.32 Million for Beverly Hills Cop in today's dollars.

You can get the CPI hot off the press from the Bureau of Labor Stats here.

Clearly, the Hangover has a way to go before it trounces Eddie Murphy.

However, I have to say that the Hangover was pretty much the funniest movie I have seen in a long long time.

The question remains hwoever, why don't journalists pay attention to inflation?

Of course, these numbers are like apples and oranges. The CPI in 1984 was 105.3 today it is 215.693. To convert BHC to todays numbers we multiply 234 by 215.693 and divide by 105.3. This gives us a whopping $479.32 Million for Beverly Hills Cop in today's dollars.

You can get the CPI hot off the press from the Bureau of Labor Stats here.

Clearly, the Hangover has a way to go before it trounces Eddie Murphy.

However, I have to say that the Hangover was pretty much the funniest movie I have seen in a long long time.

The question remains hwoever, why don't journalists pay attention to inflation?

Textbook Economics

Ever wondered what goes in to the price of a text book? Greg Mankiw's econ book gets the once over here. And a little more here.

HT: Newmark's door

HT: Newmark's door

Monday, July 20, 2009

Robert Shiller on sub primes...

Robert Shiller talks about sub prime mortgages here. He argues that a consumer protection agency should promote plain vanilla debt products for consumers - including sub prime loans. I think this is quite reasonable. In the same way that the junk bond market was hugely successful by financing lower credit quality borrowers, the sub prime loan market can also be successful and fill a gap in the market place. The key is to ensure that those making the loans fully bear the risk of the loans that they are making, and that those taking the loans fully understand the terms.

Felix Salmon disagrees and thinks this is a bad idea. But I think Felix is off the mark here. His criticisms of Shiller's argument are all based on sub prime borrowers getting loans that they couldn't repay. A transparent sub prime market where lenders bear risk would reduce the chance of this happening.

Felix Salmon disagrees and thinks this is a bad idea. But I think Felix is off the mark here. His criticisms of Shiller's argument are all based on sub prime borrowers getting loans that they couldn't repay. A transparent sub prime market where lenders bear risk would reduce the chance of this happening.

Monday, July 13, 2009

The end of asset allocation?

Felix Salmon blogs that asset allocation is dead. He argues that the basic idea of spreading your risks across asset classes with low correlations isn't working anymore, in part due to commodity ETFs being bought up by investors in the name of diversification. Apparently, this action brought the correlation between equities and commodities closer to 1.

I don't really buy this whole, "the correlations have gone to 1" argument. First of all Felix states that correlation is impossible to measure and cites a wired article about the Gaussian Copula. This is a bit of a straw man. Correlation isn't hard to estimate at all. Felix's second point is that correlation is backward looking and therefore no good. I agree that it is a backward looking measure, but I wouldn't through the baby out with the bath water quite yet.

You have to consider what are the alternatives there are to asset allocation. Felix states:

Asset allocation is not a trading or market timing strategy which might loose its ability to generate returns over time. Asset allocation is a method of managing risk. It will reduce portfolio risk overall, but as we have seen, in severe events, correlations do not necessarily go to 1, instead the impact of the market component on diverse assets becomes far more important. Nothing except being in cash would have saved you in the recent market drop, but for most time periods, asset allocation has and will continue to reduce portfolio risk. Put another way, if you are driving a car a seat belt (asset allocation) will help a lot, most of the time. But there are times when it won't (i.e. you drive off a cliff). That still doesn't mean that you shouldn't wear a seat belt.

I don't really buy this whole, "the correlations have gone to 1" argument. First of all Felix states that correlation is impossible to measure and cites a wired article about the Gaussian Copula. This is a bit of a straw man. Correlation isn't hard to estimate at all. Felix's second point is that correlation is backward looking and therefore no good. I agree that it is a backward looking measure, but I wouldn't through the baby out with the bath water quite yet.

You have to consider what are the alternatives there are to asset allocation. Felix states:

In investing, nothing lasts forever. And the era of asset allocation is in its waning years. The problem, of course, is that no one has a clue what might replace it.

Asset allocation is not a trading or market timing strategy which might loose its ability to generate returns over time. Asset allocation is a method of managing risk. It will reduce portfolio risk overall, but as we have seen, in severe events, correlations do not necessarily go to 1, instead the impact of the market component on diverse assets becomes far more important. Nothing except being in cash would have saved you in the recent market drop, but for most time periods, asset allocation has and will continue to reduce portfolio risk. Put another way, if you are driving a car a seat belt (asset allocation) will help a lot, most of the time. But there are times when it won't (i.e. you drive off a cliff). That still doesn't mean that you shouldn't wear a seat belt.

Damodaran's blog

Aswath Damodaran, an NYU finance Prof is a well known expert on valuation and corporate financial policy. Prof Damodaran has a blog here. Well worth reading. I'll be adding it to my blog reader.

FinanceProf posts a video of one of Damodaran's lectures with the great tag line "dividends are like getting married, buybacks are like hooking up".

FinanceProf posts a video of one of Damodaran's lectures with the great tag line "dividends are like getting married, buybacks are like hooking up".

stocks for the long run?

Greg Mankiw blogs on a recent article in the WSJ about some of the problems with the thesis that stocks are for the long run - i.e. that they consistently beat other asset classes.

Turns out, some of the data for the first 100 years or so was perhaps a little shaky.

Turns out, some of the data for the first 100 years or so was perhaps a little shaky.

Friday, July 10, 2009

I have a new fave blog

Check out http://self-evident.org/. Particularly the Bond Crash/Course section. Great stuff on the mechanics of swaps and loads of other goodies.

Finding this stuff interesting is a sign that you are a true finance geek! For example, the most recent post explains how you can extract inflation expectations from swaps. Brilliant stuff!

Finding this stuff interesting is a sign that you are a true finance geek! For example, the most recent post explains how you can extract inflation expectations from swaps. Brilliant stuff!

Thursday, July 9, 2009

How to deal with foreclosures

The Economist reports on a recent Fed study that tries to explain why so few mortgages that are in default are renegotiated. Turns out, it is not really because of securitization. Instead, banks tend to be reluctant to renegotiate because a) many renegotiated loans end up defaulting anyway and b) some loans that are in default "cure themselves" - in other words - come out of default. So more often than not, not doing anything is the best strategy.

Wednesday, July 8, 2009

Did Diversification Fail When We Needed It Most?

Ken French talks about diversification

Ken argues that the observation that correlations across asset classes went up recently is "probably a mis-perception". He argues that really what is happening is that the market component of risk became more significant, and to the extent that all assets have a market component, they will all be affected by this component.

However, at the end of the day, for an individual investor this is probably semantics. Pretty much everything went down!

Ken argues that the observation that correlations across asset classes went up recently is "probably a mis-perception". He argues that really what is happening is that the market component of risk became more significant, and to the extent that all assets have a market component, they will all be affected by this component.

However, at the end of the day, for an individual investor this is probably semantics. Pretty much everything went down!

Tuesday, July 7, 2009

Pope calls for new economic system

The Washington Post today reports that the Pope has weighed in on the current financial situation. He bemoans that:

I think the Pope is a little off the mark here. There is actually tremendous social value in an enterprise whose goal is to maximize shareholder wealth. First, millions of us rely on these firms to create wealth for our retirement. Second, maximizing shareholder wealth often results in greater resources being available for charitable work - take the Bill and Melinda Gates foundation for example. Third, the free market system in which capital flows to the most productive use is responsible for the improvement of the lives of millions - through medical advances, technology etc.

I don't think that this is the first time the Pope has been off the mark, but this is a finance blog so we won't go there.

"Without doubt, one of the greatest risks for business is that they are almost exclusively answerable to their investors, thereby limited in their social value."

I think the Pope is a little off the mark here. There is actually tremendous social value in an enterprise whose goal is to maximize shareholder wealth. First, millions of us rely on these firms to create wealth for our retirement. Second, maximizing shareholder wealth often results in greater resources being available for charitable work - take the Bill and Melinda Gates foundation for example. Third, the free market system in which capital flows to the most productive use is responsible for the improvement of the lives of millions - through medical advances, technology etc.

I don't think that this is the first time the Pope has been off the mark, but this is a finance blog so we won't go there.

Monday, July 6, 2009

Evil market jargon?

Jack Hough writes about evil market jargon such as "alpha" "beta" and "second derivative".

Jack doesn't think that we should use such words as they are hard to understand. He suggests instead the following....

Jack goes on to say about beta..

Uh, I don't think that's right actually. But I hate to throw the "covariance" word in to the mix given the tone of the article.

Excellent stuff. Mr Hough's columns are brilliant comic relief.

Jack doesn't think that we should use such words as they are hard to understand. He suggests instead the following....

Legally, I can’t recommend that you use it to punish those who use the four self-important terms below. That said, if you hear someone use one of the terms, and if you happen to be standing behind them, and if you love America and you’re not holding a dangerously hot coffee at the time (or if it at least has a lid), I think we both know what needs to be done

Jack goes on to say about beta..

In one common but flawed approach, a stock’s risk is defined by its past trading volatility.

Uh, I don't think that's right actually. But I hate to throw the "covariance" word in to the mix given the tone of the article.

Excellent stuff. Mr Hough's columns are brilliant comic relief.

How maths killed Lehman

A cute article written by an Oxford Ph.D. in Mathematics. (Note to US readers - Maths is the English way of saying "Math".) The article explains nicely how cross-asset-correlation, and the faulty assumption of independence of bad events could be seen as an explanation for Lehman's demise.

The online magazine "Plus - living mathematics" has a few other nice articles related to finance...

What does a financial engineer do?

How to price derivatives

and is Maths to blame?

The online magazine "Plus - living mathematics" has a few other nice articles related to finance...

What does a financial engineer do?

How to price derivatives

and is Maths to blame?

Rolling Stone: Blame Goldman Sachs

I haven't had a chance to wade through this one, but Rolling Stone has a long article on how Goldman has had its fingers in every major bubble in recent history.

Felix Salmon, also reviewed the article and found much to agree with.

Finally, Felix gets a response from GS.

I have to say though that Mr Salmon's stock went down a bit with me after he referred to vegans as "bonkers".

Anyhow, good stuff if you've got some spare time to read it all.

Felix Salmon, also reviewed the article and found much to agree with.

Finally, Felix gets a response from GS.

I have to say though that Mr Salmon's stock went down a bit with me after he referred to vegans as "bonkers".

Anyhow, good stuff if you've got some spare time to read it all.

Is the worst over?

According to NPR, "most" economists think so. Unfortunately, what really matters is that most consumers think so too.

Federal debt and the level of interest rates

Econ 101 states that as the federal debt grows, interest rates will rise and this will have a crowding out effect on private investment. A recent article suggests that this might happen.

Thursday, July 2, 2009

Behavioral economics / finance

Behavioral economics (and finance) has fully matured into its own sub-field. In essence, it examines how psychological factors influence the behavior of participants in various markets.

It is important to distinguish between the behavior of people reacting to incentives, which might seem irrational, and true behavioral factors. In the book "Freakonomics" there is a section on a day care center which tried to deal with tardy parents picking up their kids by imposing a fine on late pickups. The result - more late pickups, because the fine was less than the hourly cost of daycare, and parents rationally responded to the offer of this "after hours" care. This is not really an example behavioral economics.

An example of behavioral finance is the 1/n rule. If you give people "n" choices - say 4 mutual funds in their retirement plan, folks will tend to put 25% of their money in each fund, when optimally a different allocation is probably best.

Anyhow, Scientific American has a piece on how bubbles develop.

The article first talks about "money illusion" a topic close to my heart as this was the focus of my PhD dissertation and subsequent publication in the Journal of Financial and Quantitative Analysis. Money illusion occurs when individuals fail to appreciate the effects of inflation on asset values. To quote from the article:

The article goes on to cover several other well documented examples of behavioral irrationality. Overall an excellent read.

It is important to distinguish between the behavior of people reacting to incentives, which might seem irrational, and true behavioral factors. In the book "Freakonomics" there is a section on a day care center which tried to deal with tardy parents picking up their kids by imposing a fine on late pickups. The result - more late pickups, because the fine was less than the hourly cost of daycare, and parents rationally responded to the offer of this "after hours" care. This is not really an example behavioral economics.

An example of behavioral finance is the 1/n rule. If you give people "n" choices - say 4 mutual funds in their retirement plan, folks will tend to put 25% of their money in each fund, when optimally a different allocation is probably best.

Anyhow, Scientific American has a piece on how bubbles develop.

The article first talks about "money illusion" a topic close to my heart as this was the focus of my PhD dissertation and subsequent publication in the Journal of Financial and Quantitative Analysis. Money illusion occurs when individuals fail to appreciate the effects of inflation on asset values. To quote from the article:

Robert J. Shiller, a professor of economics at Yale University, contends that the faulty logic of money illusion contributed to the housing bubble: “Since people are likely to remember the price they paid for their house from many years ago but remember few other prices from then, they have the mistaken impression that home prices have gone up more than other prices, giving a mistakenly exaggerated impression of the investment potential of houses.”

The article goes on to cover several other well documented examples of behavioral irrationality. Overall an excellent read.

Bond data online

FINRA now has bond data online. You can find some of this on yahoo finance, but this is a particularly nice setup.

HT: Felix Salmon

HT: Felix Salmon

Tuesday, June 30, 2009

The value of a college degree - an example of bad math

The New York Post (not a renowned source for financial analysis) has an article by Jack Hough (an editor at "smart money") that argues that a college degree isn't worth the money.

The article also shows up here on the smartmoney website.

In finance lingo, he is saying that a college degree is a negative net present value project. At first blush it looks like he has a point. The first page of the article gives the example of two individuals. One starts work and the other goes to college and assumes a college loan. Mr Hough goes on to show that at retirement, the college grad will have about 1/3 of the wealth in his retirement account as his non-college going buddy.

Mr Hough then goes into a rather unfocussed rant explaining the reason for this - that basically professors are useless and we don't teach anything of value....

I smelled a rat.

Unfortunately the math in the example is completely wrong. The example assumes that both put aside 5% of their income to either retirement or paying down loans.

At age 22 the non-college guy will have a net pay of 16055 (assuming income growth and his 5% retirement payment).

The college guy on the other hand has a net pay of 22,329 after he has paid 5% of his salary to his loan (Mr Hough's assumption).

The example completely ignores the difference in their net pay, i.e. $22,329 - $16,055 = $6,274. It is implicitly assumed that college guy just spends this. But if he lived on the same net pay as the non-college guy, you can show that he'd pay of his loan in 3 years and retire with $3.4M (about 2.5 times as much as the non-college guy).

Now, in fairness to Mr Hough, he does note that:

But this is precisely the point! You have to look at total earnings, not just some arbitrary percentage of earnings. The difference in the two living standards is likely to be massive.

In my analysis, I assumed that this would all be invested by the college grad, but we could just assume that he'd invest enough to retire at an equal level with his non-college pal, and then enjoy the rest during his life.